Over the years, Real Estate Investment Trusts (REITs) have become a popular real estate investment vehicle. Approximately 145 million Americans, or roughly 44% of American households, invest in REIT stocks. The benefits are many: high dividends, low volatility, and consistent cash flow in the form of ordinary dividends. But one of the most appealing to investors is REIT tax benefits. Let’s talk about some of the most important ones.

What is a REIT?

A REIT or a Real Estate Investment Trust is an investment company that purchases and owns income-producing real estate. REITs invest in both residential or commercial real estate and provide income to shareholders in the form of dividends. Each unit in a REIT represents proportional ownership of the properties and similar to a mutual fund, it’s helpful to look at past performance to get a sense of future results.

To qualify as a REIT, a company must:

- Invest at least 75% of its total assets in real estate.

- Derive at least 75% of its gross income from rents from real property, interest on mortgages financing real property or from sales of real estate.

- Pay at least 90% of its taxable income in the form of shareholder dividends each year.

- Be an entity that is taxable as a corporation.

- Be managed by a board of directors or trustees.

- Have a minimum of 100 shareholders.

- Have no more than 50% of its shares held by five or fewer individuals.

The three categories of REIT

REITs can be classed into three main categories based on how they’re purchased. These include:

Publicly traded REITs

These REITs are traded on major stock exchanges and can be purchased by individual investors with ordinary brokerage accounts. Since they’re traded on the NYSE and the NASDAQ exchange, publicly traded REITs are regulated by the U.S. Securities and Exchange Commission (SEC) and must provide audited financial reports. There are currently more than 200 publicly traded REITs available on the market.

Public non-traded REITs

Like stock exchange-listed publicly traded REITS, public non-traded REITs are required to register with the Securities and Exchange Commission, but do not trade on major securities exchanges. Public non-traded REITs operate like publicly traded REITs in almost every way except that they face redemption restrictions that limit their liquidity. There is generally a minimum holding period for public non-traded REITs. They are also required to provide quarterly and yearly financial reports. Long-term rentals on Arrived are structured as public non-traded REITs (note: Vacation rentals are considered ‘active’ income and, therefore, not REIT eligible. Please see your tax advisor for specific investment advice).

Private non-traded REITs

Private REITs are not traded on a national stock exchange and are exempt from SEC regulations, which means they are not subject to the same disclosure requirements as those listed on the stock exchange or public non-traded REITs. Private non-traded REITs are typically sold only to institutional investors, such as large pension funds or accredited investors, defined as individuals with a net worth of at least $1 million or an annual income exceeding $200,000.

The three types of REITs

Within those three categories, REITs generally fall into three broad types:

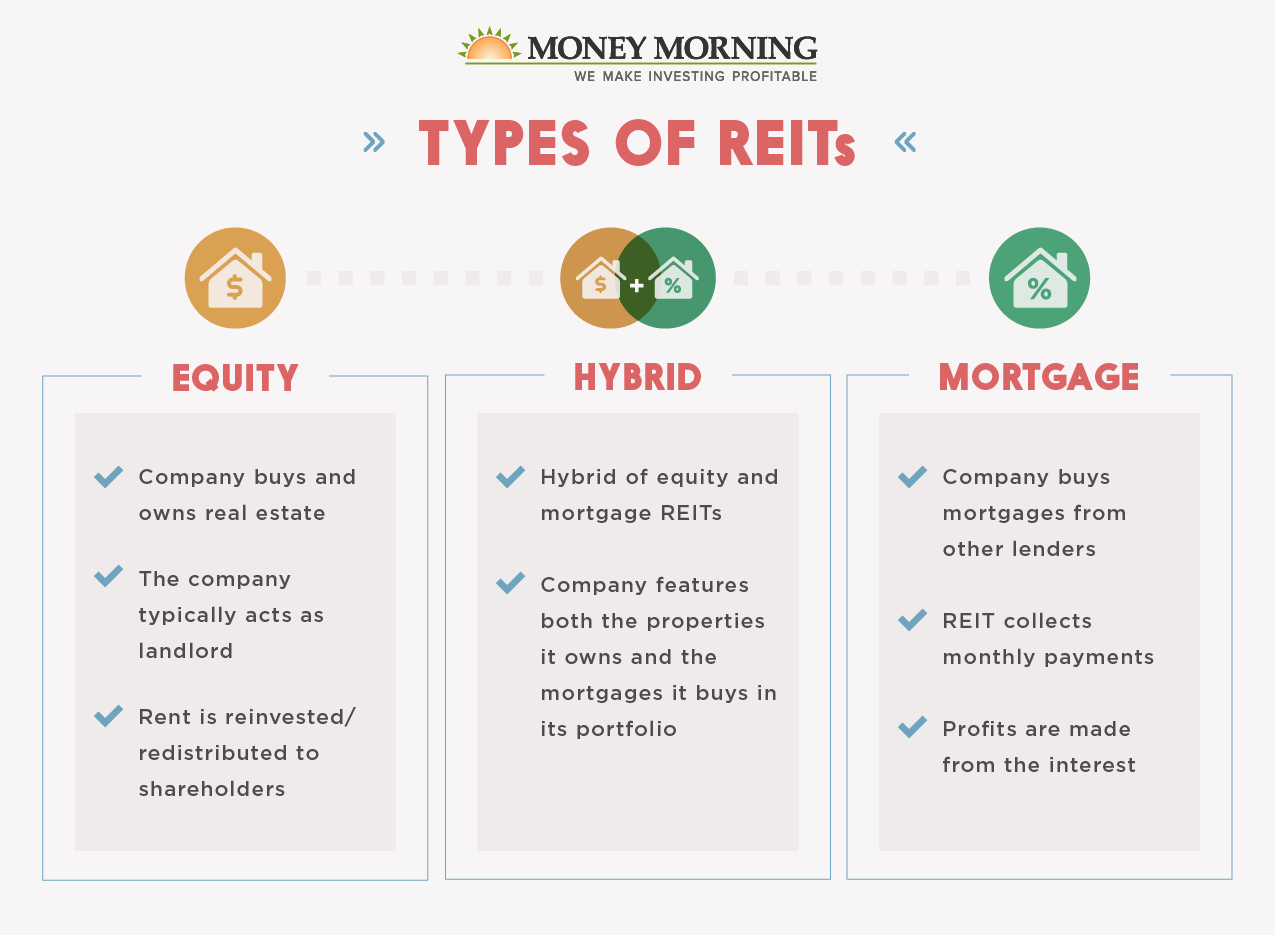

Equity REITs

These are real estate trusts that derive their income from three sources: rental income, dividends, and capital gains from property sales. Equity REITs also referred to as eREITs, focus on building, developing, managing, repairing, and sometimes selling investment property.

The properties held and managed by this type of REIT can be both residential or commercial in nature and include single or multi-family homes, apartment complexes, commercial buildings, office spaces, storage buildings, and shopping centers. Investors are not responsible for the day-to-day management of real estate assets.

Mortgage REITs

These REITs invest in mortgages and mortgage-backed securities. What this means is that a mortgage REIT or mREIT doesn’t actually own any physical assets. Instead, it originates or purchases mortgages or mortgage-backed securities in residential or commercial properties.

The mortgages earn interest from borrowers and investors earn an income in the form of dividend distributions. Mortgage REIT shares offer high dividends. However, owing to the nature of lending, they are easily impacted by rising and falling interest rates.

Hybrid REITs

These REITs combine mortgage and equity investments and hold both real estate and mortgages. They can be a good option for investors who want to minimize risk and dependence on market trends. Like the other two, hybrid REITs can be publicly or privately traded and are considered fairly liquid investments. They generate income from both tenant rental payments as well as loan interest.

The tax benefits of REITs

One of the reasons REITs are so appealing to investors is that they offer a number of tax advantages not available to other asset classes. Taxation with REITs can get somewhat complicated since each dividend payout can comprise a combination of funds from a range of sources and categories.

For example, while the bulk of REIT dividend payouts consists of a company’s operating profit that is taxed as non-qualified dividends, sometimes they include a portion of operating profit that was previously sheltered from tax due to depreciation. This would now be considered a nontaxable return of capital (ROC). Dividends may also consist of capital gains, which would incur short or long-term capital gains tax based on how long the REIT company owned that asset before it was sold.

We advise working with a financial advisor to file your tax return and for tax advice to make sure you understand the tax consequences of your REIT investments. Here are two that are worth understanding.

Pass-through taxation

The primary tax benefit of a REIT is the avoidance of what is called “double taxation,” that is, the payment of corporate tax and personal tax on the same income. Broadly speaking, a company is first taxed at the corporate level and, when that income is distributed to investors, it is taxed again on a personal level.

However, most US businesses are not subject to corporate income tax. Instead, their profits flow through to owners or members and are taxed under the individual federal tax. As per the IRS, these pass-through businesses include sole proprietorships, partnerships, limited liability companies, and S-corporations.

REITs are also pass-through entities, which means they don’t pay a corporate income tax and investors get to keep more of their earnings.

Here is how the flow of money works in a corporation:

- The corporation earns money and calculates its profit after expenses.

- It pays a corporate income tax to the federal government.

- The remaining profit is distributed to investors as dividends.

- Investors receive dividends and pay personal tax on that income.

Here is how it works with a REIT:

- The corporation earns money and calculates its profit after expenses.

- The profit is distributed to investors as dividends.

- Investors receive dividends and pay personal tax on that income.

With REIT distributions, there is no corporate tax, which means that money that corporations send to the federal government is instead distributed among investors, putting more in their pockets.

Qualified Business Income deduction

REITs were created in 1960 as an easy and tax-effective way for people to invest in real estate. In 2017, the Tax Cuts and Jobs Act (TCJA) put even more power in having a REIT status by making them incredibly tax efficient.

Part of what the TCJA does is give a special tax break, called the QBI (Qualified Business Income) deduction, to owners of passthrough entities. This allowing them to deduct 20% of their income, thereby effectively taxing only 80% of the qualifying income. Since REITs are passthrough businesses, investors in REITs are only taxed on 80% of their dividend income.

It’s important to note, however, that not every company qualifies for the QBI deduction. In addition to being a passthrough entity, a company cannot be a “specified service trade or business,” which usually includes doctors, dentists, and lawyers.

Arrived’s investments, which qualify as passthrough entities and meet all the requirements to qualify for this deduction, benefit from the QBI tax break. This means that by investing in REITs like Arrived, investors are able to keep 20% of their dividend income tax-free.

A hypothetical example of REIT taxation

To bring this all into perspective, let’s use a hypothetical example to illustrate how much more money these tax savings will put in your pocket in a single tax year.

To keep it simple, let’s assume a profit of $1,000 is to be distributed among each REIT investor. Now, thanks to our REIT being a passthrough entity, it is not subject to a corporate tax rate of 21%, which means that the entirety of that (21% * 1000 = $210) can be passed on to investors.

Assuming investors are in the 24% income tax bracket for their ordinary income, that means each investor would pay $240 (24% * 1,000 = $240) in taxes and be left with $760.

However, because of the QBI, there is a further 20% deduction available to investors, which means that instead of paying the 24% income tax rate on $1,000, they’d pay it on $800.

So, instead of paying $240 in tax, they pay $192 on their REIT income.

In total, the deductions allow for the investor to keep $258 more than they otherwise would have. For dividends that contain capital gain, they would be taxed at separate, lower capital gains rates.

Easily invest in rental homes

REITs provide a steady source of income as well as tax advantages that let you keep more of that money in your pocket. Arrived long-term rental homes are structured as public non-trading REITs, which means investing in real estate through Arrived not only allows you to get started without the hassle of finding and managing real estate but also take advantage of the multiple benefits for taxpayers that investing in REITs allows. Ready to get started building your real estate portfolio? Take a look at some of the properties we have on offer here.

The opinions expressed in this article are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. The views reflected in the commentary are subject to change at any time without notice. View Arrived’s disclaimers .